[ad_1]

Auto demand levels expected to continue tapering from 2Q

results

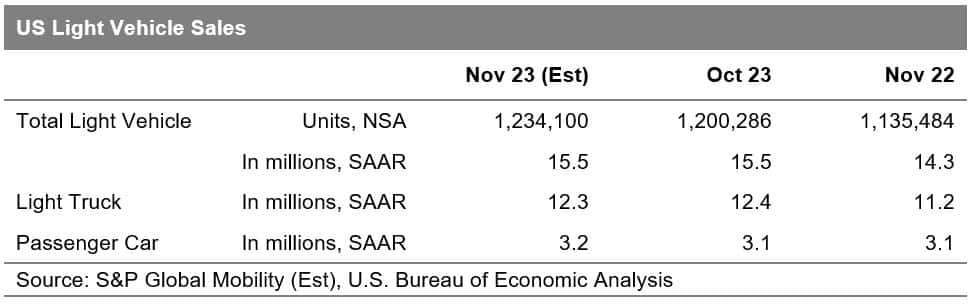

On an unadjusted volume level, November US light vehicle sales

are expected to advance mildly from the strike impacted levels of

October but remain absent of any momentum. S&P Global Mobility

projects sales volume of 1.23 million units for November, which

would translate to a seasonally adjusted sales rate (SAAR) of 15.5

million units for the month, even with the month-prior level.

“While the end of the UAW strikes provides some potential relief

to those automakers impacted, the ever-present affordability

concerns remain prevalent for the foreseeable future,” reports

Chris Hopson, principal analyst at S&P Global Mobility. “Over

the course of the next few months, it’s difficult to imagine auto

sales getting a jump start from the current pace of demand, with

the upshot being a bounce in early 2024 production creating a

progression for inventory and incentive levels to develop come

spring of 2024.”

New vehicle retail advertised

inventory listings peaked in mid-October just shy of 2.5

million units and have seen a slight decrease since then – from an

end-of-October level of 2.35 million units to about 2.3 million in

mid-November.

“As of mid-October, there was still more advertised dealer

inventory of outgoing 2023 model year models than incoming 2024s,

and the 2024 model year inventory was growing at a faster rate than

the 2023 model year sell-down,” said Matt Trommer, associate

director of Market Reporting at S&P Global Mobility. “But as of

mid-November, that tide seems to have reversed; there are now fewer

2023s (about 955,000 units) than 2024s (about 1.34 million).”

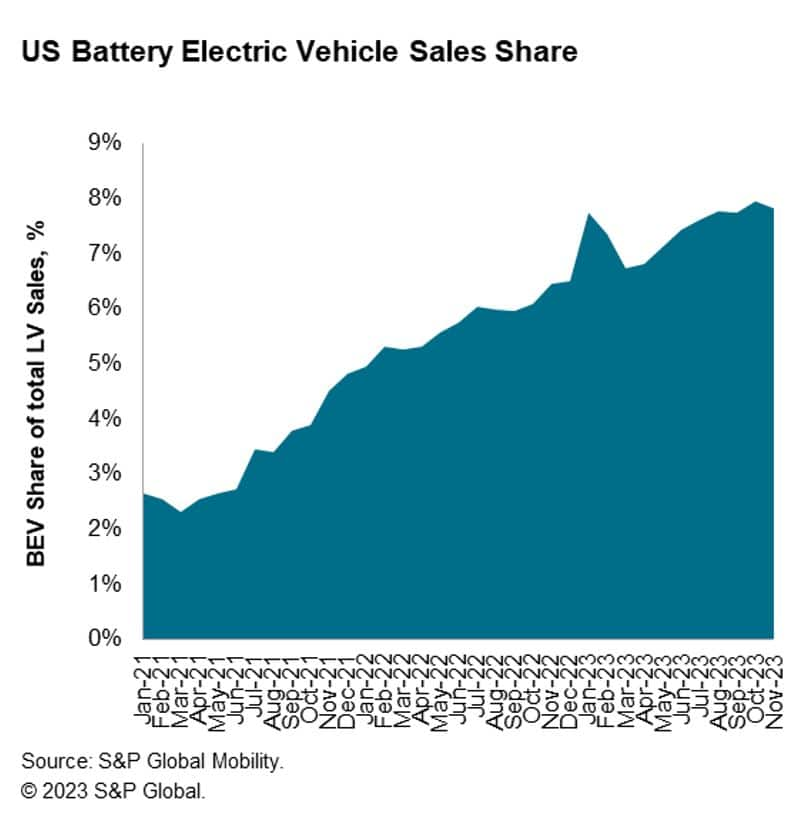

Continued development of battery-electric vehicle (BEV) sales

remains an assumption in the longer term S&P Global Mobility

light vehicle sales forecast. In the immediate term, some

month-to-month volatility is anticipated. October 2023 BEV share is

expected to reach 7.8%, similar to the month prior reading and

pushing year-to-date BEV sales growth to an estimated 47%. BEV

programs previously expected for stronger launches in Q4 2023 have

been delayed to 2024, creating opportunity for BEV share advances

beginning early next year.

Electric vehicle retail advertised inventories (not including

Tesla) also peaked in mid-October at 135,000 units and have

declined slightly since then. Most BEV nameplates have reached an

inventory plateau and flattened off.

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.

[ad_2]