[ad_1]

LISTEN TO A PODCAST ON THIS TOPIC

WITH S&P GLOBAL MOBILITY EXPERTS

With internal-combustion and battery-electric

vehicles vying for showroom space and advertising dollars, peak

model complexity will transform marketing messaging and media

spend.

Today, US auto shoppers have nearly 450 vehicle

nameplates to consider. Within five years, that number will grow

considerably. With the arrival of electric vehicles across every

mainstream and luxury brand, approximately 650 models will be

competing for showroom space, lot space, digital space, marketing

budget and most importantly, customer attention. This isn’t just a

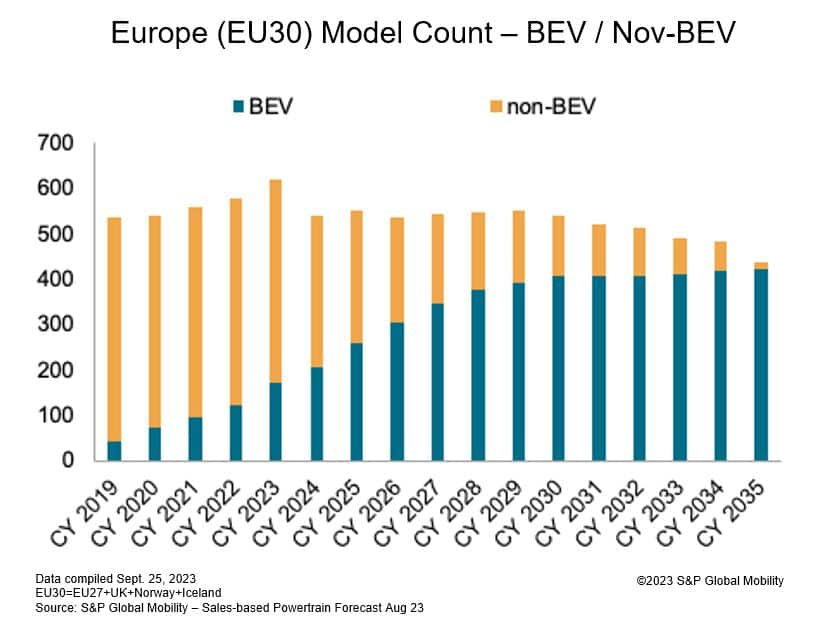

US phenomenon; a similar equation will happen in the European

market — perhaps more so, as mainland Chinese automakers are

already launching their EV-minded brands there as well.

It’s hard enough for consumers to keep track of

all the various vehicles vying for headspace with a portfolio that

mostly comprises internal-combustion engine (ICE) vehicles. But the

push for electrification is about to escalate that consumer

confusion. How automakers and their advertising agencies respond to

this challenge will determine how effectively — and profitably

— they manage the transition from ICE to battery-electric

vehicle (BEV).

As early as 2026, S&P Global Mobility

expects the total of new EV models available to break 200 in the US

market, as the ICE new model count continues a steady decline. In

late 2027/early 2028, the total model count should be at its apex

— with the number of options across all propulsion system

designs approaching 650. The situation will be just as dramatic in

Europe.

S&P Global Mobility refers to this

situation as Peak Model Complexity — and its impact on

marketing throughout the funnel, across all initiatives, will be

transformative.

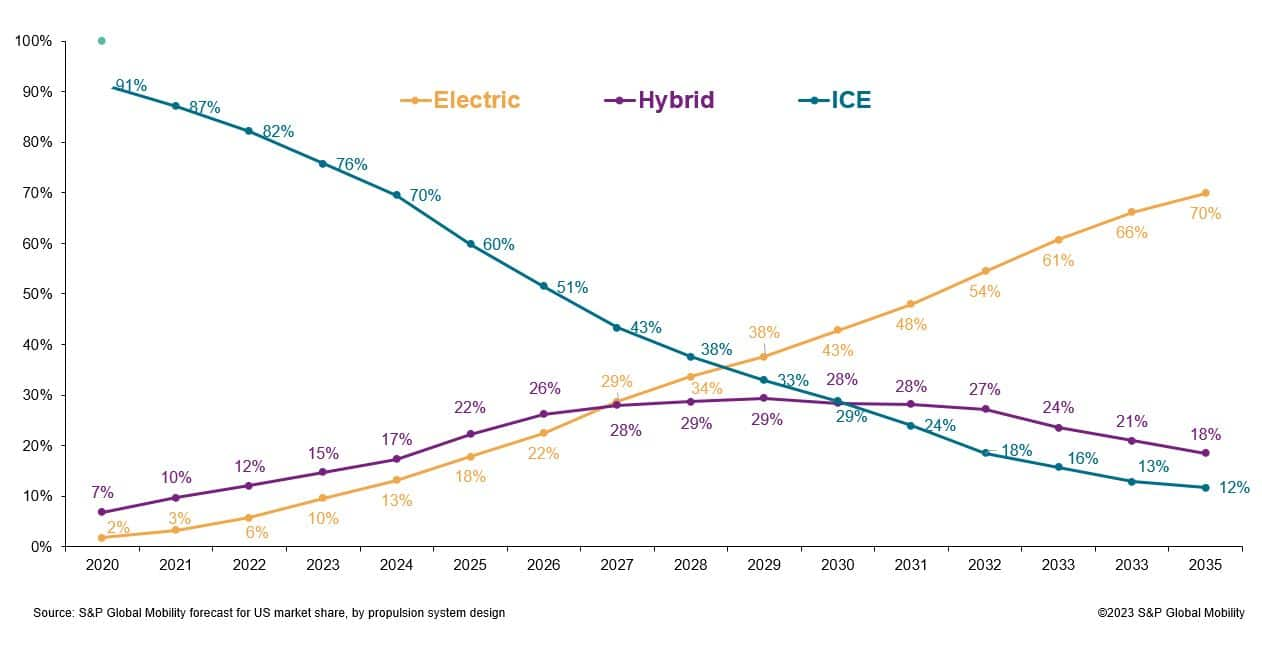

Market share parity by

2028

S&P Global Mobility forecasts that the

three propulsion system designs — EV, hybrid, and ICE —

will each account for between 29% and 36% market share by the end

of this decade. After that, EV share is expected to continue to

grow while hybrid plateaus and then joins ICE in a continuous, but

slow, decline.

The increased model count will cause a drop in

sales-per-nameplate figures: In 2018, the average sales volume per

nameplate in the US market was 49,000 units. That is expected to

dip to 36,000 by 2027. This requires some new thinking by OEMs,

which for decades have stated that a nameplate must sell between

40,000 and 60,000 units to be profitable.

But this tectonic shift is happening already

— impacting production cycles, sales forecasting, supplier

relationships and marketing budget allocation.

The impact to profit margins, platform

economics, operating expenses, product lifecycles and go-to-market

timing will cut across all aspects of the auto business — from

new and used car sales, to vehicle acquisition, parts and service.

Retailers and their marketers will need to do more with less, and

sooner than later.

Every marketing campaign and initiative will

face this decision: Which message or offer should we serve to which

customer — EV, hybrid, or ICE?

Obviously, big-hitter vehicles like the Ford

F-150 and Toyota RAV4 will continue to have strong marketing

budgets. But if a company is adding four or more new electric

nameplates, and not deleting any internal combustion vehicles, they

need to decide if there will be an incremental spend, or if some

vehicle’s marketing budget will be adjusted.

Already, many OEMs employ a “fire-and-forget”

marketing strategy, where a new-product launch gets a big spend,

but then ad dollars wither until a sales event comes along.

Automakers are already stretched thin on covering their existing

ICE model lines; what happens to the strategy when a slew of EVs

— and an EV branding campaign — are added to the mix?

The situation may be even more accelerated in

the European market, as the swing from ICE to BEV is already well

underway. However, it seems the number of ICE nameplates are being

removed from the market at the same pace as new BEVs are being

introduced. But that doesn’t eliminate the need to educate and

alert consumers to the arrival of differently named BEVs.

Brand loyalty and nomads

The recent semiconductor supply chain crisis

crimped vehicle inventories, which in turn triggered historic low

brand loyalty levels for return-to-market households. Improving

inventories have provided a rebound to those loyalty levels.

However, the effects from two years of a constrained market remain

evident, and vehicle buying behaviors changed as a result.

In US loyalty data collected in 2022, 53% of

shoppers were “nomads,” meaning

they had no brand affinity to the vehicle they disposed of or just

acquired. This rate approaches historic highs — that’s a bad

thing for OEMs — and is important as these households defect to

another brand. Nearly 6 of every 10 nomad shoppers are going to

switch brands with their next vehicle purchase.

Meanwhile, lease rates plummeted in 2022 to

less than 18% of new vehicle sales, down from 30% in 2018. This

drop translates to about 1.5 million fewer households that are

regularly returning to market. And lease returns are some of the

most brand loyal and valuable customers when considering:

-

64% brand loyalty for lease households versus

46% for those that purchase; -

63% of lease households return to market in

less than three years versus 51% for purchase households; -

Lease returns also provide a consistent flow of

certified pre-owned stock, which provides a loyalty lift of 8

percentage points for brands over those that buy.

Electrification and the shift to

luxury

Over the last five years, US consumers have

increased their purchases of luxury-badged vehicles — which now

account for 20% of sales, up from 13.5% in 2018, according to

S&P Global Mobility registration data analysis.

While luxury vehicles have higher profit

margins and more add-on features, it’s a crowded marketplace. There

are nearly as many luxury brands (22) competing for 20% of the

market, as there are mainstream brands (27) competing for the other

80%. As a result, luxury brands have the lowest loyalty rates. Even

with the “Tesla bump” for its industry-leading loyalty, luxury

still trails the industry average by nearly 7 percentage points.

Conquesting opportunities exist for those brands and dealers that

can leverage purchase triggers like loyalty behavior, lease term

and buying preferences.

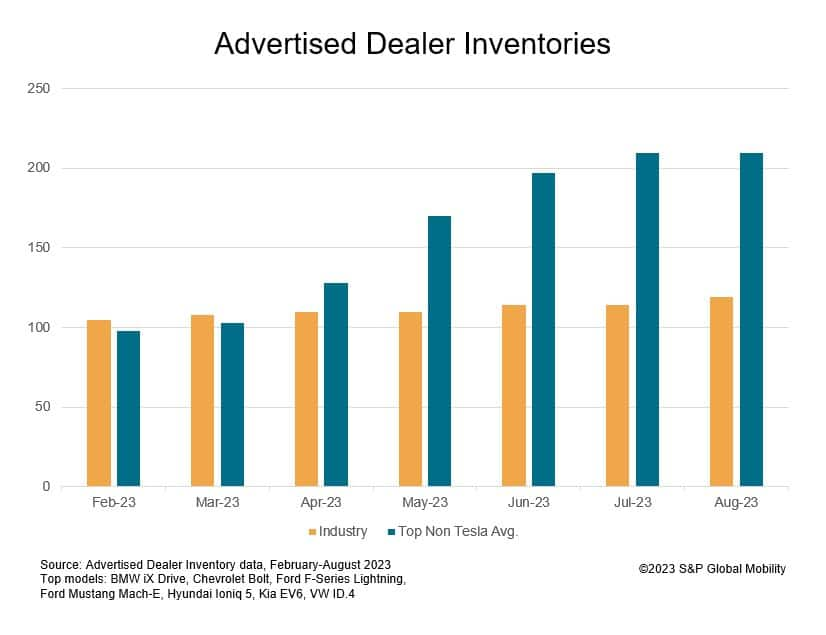

BEVs — already benefiting from the largest

increases in marketing support during the constrained market —

will continue to receive a huge chunk of media spend over the

course of this decade for new model launch support.

This imbalance of media spend versus market

share is starting to play out in days’ supply and incentive offers

as several EV models are currently at the top of both categories.

Looking at inventories for all EVs (except for Tesla) through the

first eight months of 2023, we can see advertised dealer inventory

levels for these popular models, on average, are growing twice as

fast as the rest of the industry.

EVs also remain a mostly additive purchase,

with 7 in 10 joining other vehicles in the driveway instead of

replacing one, according to S&P Global Mobility analysis.

Additionally, the vehicle shortages related to the semiconductor

crisis have trained US buyers to wait. S&P Global Mobility’s 2022 Vehicle Buyer

Journey study showed that 56% of new car shoppers are willing

to wait one month to get the vehicle they want. These buying

motivations don’t align strongly with incentive messaging.

The status of EVs as replacement vehicles will

likely shift later this decade, signaling a substantial change in

buying motivations as demand starts to close the gap with marketing

spend. In the meantime, though, retailers need to develop targeted

messaging strategies for their hybrid and ICE inventory.

Managing marketing

complexity

As vehicle supply and model counts rise, so

does competition for consumer attention. Customers expect

personalization and relevant offers, and prefer to handle most of

the consideration and transaction process digitally. With different

customer types, vehicle types and buying motivations, there is

increased importance in targeted, unique and dynamic messaging.

Turning marketplace challenges into opportunity

starts here. Better personalization needs to have accurate,

actionable data. There are four important ways marketers can

develop more effective messaging, reduce waste and improve

marketing ROI:

-

Employ vehicle verification. Does the consumer

have their car? Reduce wasted impressions and stop annoying

customers with irrelevant offers by identifying vehicle

disposers. -

Enrich customer profiles. Go beyond your

customer’s most recent purchase to develop a comprehensive

household profile — including what other vehicles are owned,

financial profiles, lease information, and loyalty to a segment,

make or model. -

Resolve identity gaps from inaccurate data.

Identification data is often incomplete. Data cleansing and hygiene

reduce database management costs and improve the chances that your

message is delivered to the intended customer. -

Scale first-party assets by developing

look-a-likes from your CRM profiles. Create specific audiences as

qualified prospects and message to recruit these net-new car

shoppers into your CRM program.

Identifying and targeting the

households that matter

Better targeting and measurement are now

available within broad-reach media like TV. Auto marketers no

longer need to rely solely on demographic buying to reach customers

at scale.

Polk Audiences data shows that about 52 million

US households — about 40% of the population — regularly buy

new cars. Another 22 million own used vehicles. But 50 million

households do not own a vehicle at all — representing a vast

number of potential wasted impressions.

With the forthcoming blitz of new vehicle

launches, there will be more pressure on media budgets and

automakers’ ability to drive sales efficiently. By moving beyond

demographic targets, marketers can mitigate waste and target

households with the highest propensity to buy now.

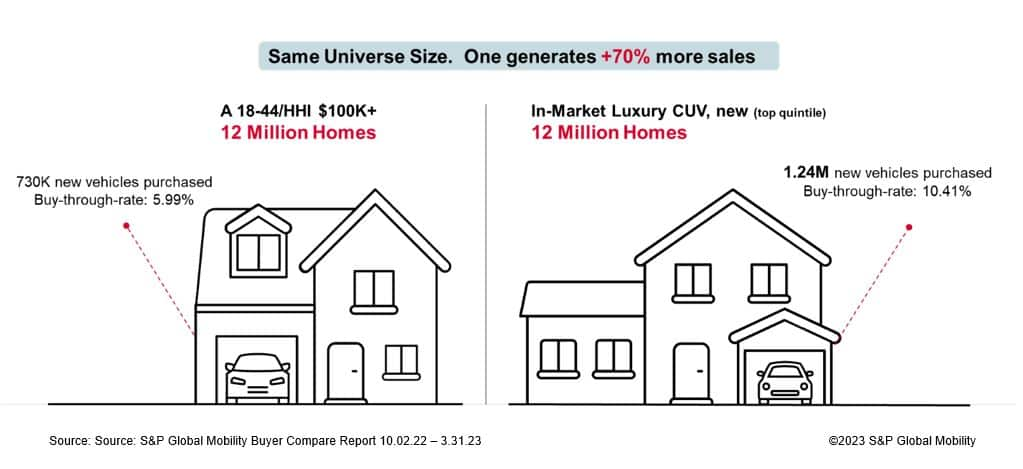

Looking into Polk Audiences In-Market segments,

OEMs and dealers can compare sales and buy-through rates to

demo-based buying audiences. In this example, we see the highly

desirable upscale, young adult demographic aged 18-44 with a

household income of more than $100,000, compared to in-market

shoppers for a luxury compact utility vehicle (CUV). They have the

same universe size of 12 million households. The addressable,

targeted approach is well positioned to deliver more sales — a

lot more sales.

Today, automotive marketers are making great

strides in leveraging technology and data science to develop

advanced audiences, messaging strategies and improved digital

communication tools. These are going to be critical for success

because, in a few tomorrows, marketers will have to manage more

customer types, vehicle types and buying motivations — all

while trying to break through 30% more competitive noise.

Authors:

Jason Jordhamo – Director, Polk Automotive Solutions, S&P

Global Mobility

Joe Kyriakoza – Vice President and General Manager, Polk Automotive

Solutions, S&P Global Mobility

————————————————————–

Dive deeper into these mobility insights:

MOBILITY INTELLIGENCE FOR AUTOMOTIVE MARKETING

THE EVOLUTION OF THE EV

CONSUMER

POLK AUTOMOTIVE SOLUTIONS

WARNING SIGNS ON THE PASS TO MASS

EV ADOPTION

VEHICLE OWNER DATABASE

SERVICES

FOR MORE ON LOYALTY AND CONQUEST

ANALYTICS

SUBSCRIBE TO OUR TOP 10 INDUSTRY

TRENDS NEWSLETTER

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.

[ad_2]