[ad_1]

LISTEN TO THIS FUEL FOR

THOUGHT PODCAST

Rising new vehicle prices in the US and Europe

are leaving cash-strapped consumers with limited options for cheap

cars – and the affordability gap is getting worse as premium-priced

electric vehicles enter the market. But as legacy automakers depart

the entry-segment, white space opportunity emerges for new,

lower-cost manufacturers to enter the fray.

In the past decade, it was possible to find an

entry-level new vehicle for less than $20,000. But pricing in the

US market has recently increased dramatically to where $25,000 or

even $30,000 is the lowest possible transaction price for a

“low-priced” vehicle. Similar activity is occurring in the European

market, in the A- and B-segments.

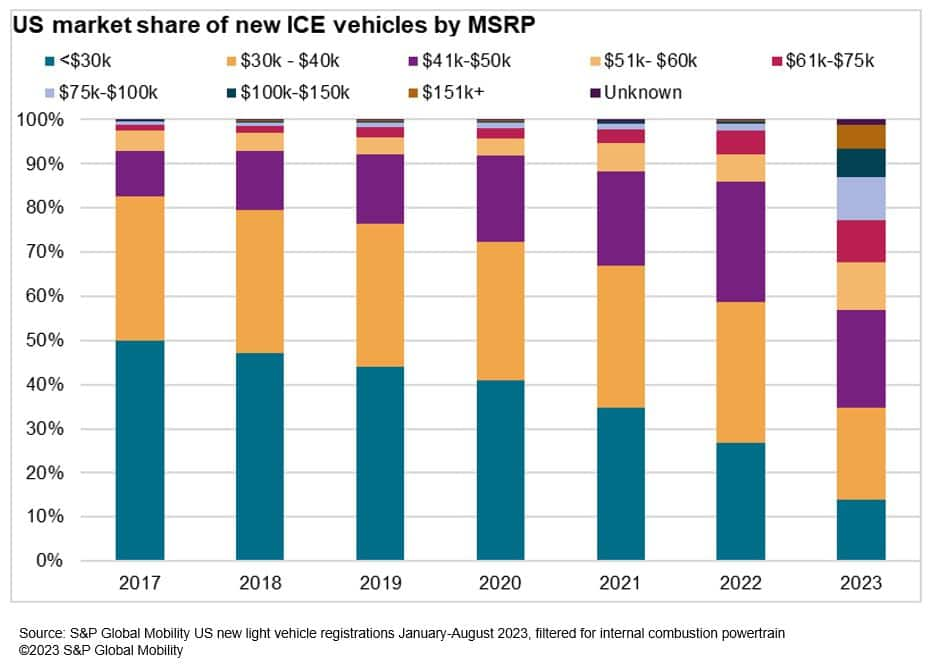

Based on S&P Global Mobility analysis of

registration data since 2017, the US market has seen a significant

decline in the share of new vehicles registered below a $30,000

price point. In just seven years, the percentage of vehicles

registered with an MSRP below $30,000 has decreased from half the

market to barely one-quarter – with vehicles in the $41,000-$60,000

band taking up nearly the entirety of that vehicle count.

For this analysis, S&P Global Mobility

classified an “affordable” vehicle in the US as one with an MSRP

below $30,000, compared to a $25,000 threshold in 2017. Even when

adjusting for inflation, comparing 2017 to 2023, the US market has

a net 16 fewer affordable models.

Notably, some vehicles that did not meet the

$25,000 threshold in 2017 are now considered affordable with the

$30,000 limit – including some trims of the Buick Encore, Chevrolet

Equinox, and Honda Accord. But that’s based on raising the pricing

bar, while consumer take-home pay has not necessarily followed suit

– which is reflected in showroom traffic. (A word about

methodology: S&P Global Mobility’s data is based on lowest

available model trim MSRP, which in this case further substantiates

the idea that vehicles have become less affordable.)

It’s more than last year’s inflationary spike

driving price hikes in the US market. Over the course of the last

decade, many OEMs who played in the lower end of the market have

simply eliminated their entry-level nameplates – examples include

the Mitsubishi Mirage, Honda Fit, Toyota Yaris, Mazda2, Hyundai

Accent, Ford Fiesta, Dodge Dart, Chrysler 200, and Chevrolet Sonic

and Spark.

Small car shortfall in

Europe

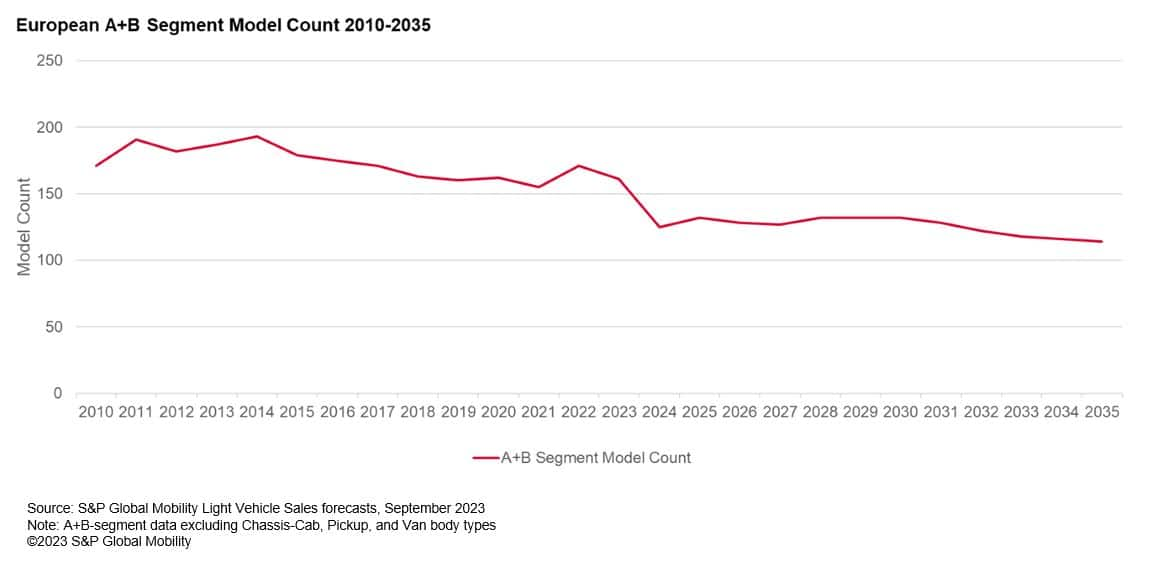

In Europe, the A- and B-segments were once

hypercompetitive hotbeds for entry-level buyers. Now those segments

are thinly populated and lightly marketed as automakers chase

growing margins in C-segment crossovers to meet growing consumer

demand. The number of A- and B-segment vehicles peaked in 2014 at

190 models, but that has since slumped to 160 in 2023 and is

predicted to decline further to 124 models in 2024 – and will

likely continue declining through 2035, according to S&P Global

Mobility forecasts.

Although many automakers cite a struggle to

make a business case with small cars, Ford had a long-time success

with its Fiesta hatchback. Despite a 47-year history, more than 20

million units sold worldwide, and – prior to the pandemic – a

perennial place among the top-selling vehicles in Europe, Ford

nonetheless deleted the Fiesta earlier this year. Other low-priced,

strong-selling vehicles departing the European scene include the

Citroen C1 and Volkswagen Up!, as well as Opel exiting the

A-segment in 2019 when it ceased production of the Adam and

Karl.

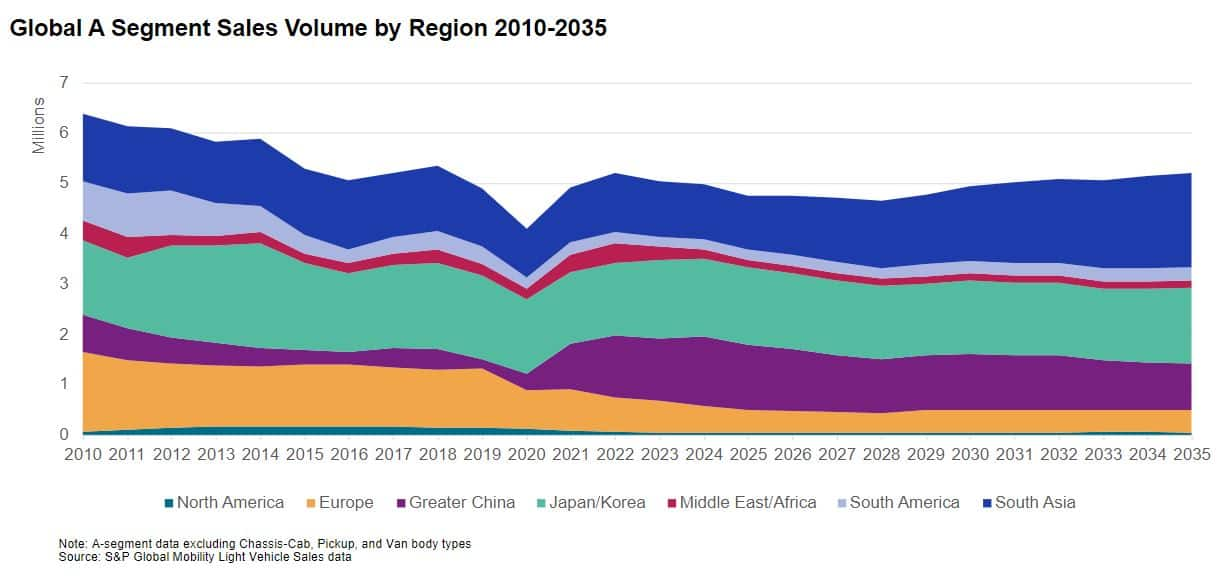

Globally, sales of A-segment vehicles have

shrunk from nearly 6.5 million units in 2010 to a predicted 5

million in 2023. S&P Global Mobility forecasts a continued

decline for the next several years – with only the South Asia

market poised for growth through 2035.

Decline of A- and B-segment cars in

Europe expected to continue

What prompted the exodus from

affordable cars?

Two years of significantly higher-than-average

nominal vehicle price growth has reduced the number of affordable

vehicle options, according to a proprietary study by S&P Global

Mobility. Price increases have been a factor of additional vehicle

content, as well as a focus on higher trim levels to maximize

profit during the low-inventory pandemic years – coupled with

regulations addressing vehicle emissions and efficiency.

Average vehicle prices began to rise above

inflation rates in 2019 as consumer demands have evolved. The

market shifted away from low-cost sedan and hatchback models toward

relatively more-expensive SUV body styles.

In the period of 2020 through 2022, supply

chain constraints pushed OEMs to prioritize higher-profit

top-trim-levels with higher content. This shifted the way OEMs

operate – including the elimination of base trim levels for

C-segment vehicles in the US – including the Ford Bronco and Honda

Civic DX (the new “base” Civic LX starts above $25,000, including

destination charges).

CAFE regulations are actually making

vehicles larger

Manufacturers began to phase out sedans as CAFE

regulations in the US became more stringent. The sleeker silhouette

of a sedan is subject to higher, more challenging targets, while

SUV-shaped crossovers – even if mounted on the same platform with

the same front-drive running gear as their sedan cousins – are

typically categorized as light trucks and thus given easier targets

to hit in fuel economy regulations.

That is a key reason sedan models such as the

Chevrolet Cruze and Ford Fusion were dropped from portfolios, while

their platform-sharing siblings Chevrolet Equinox and Ford Edge

crossovers remained.

What’s more, increasingly stringent regulations

drove rising vehicle prices as manufacturers implemented Stop/Start

or hybrid technologies to meet emissions compliance and attain CAFE

standards. Thus began the phasing out of pure ICE powertrains while

increasing the market share of more expensive hybrids and

battery-electric vehicles.

EV affordability an issue

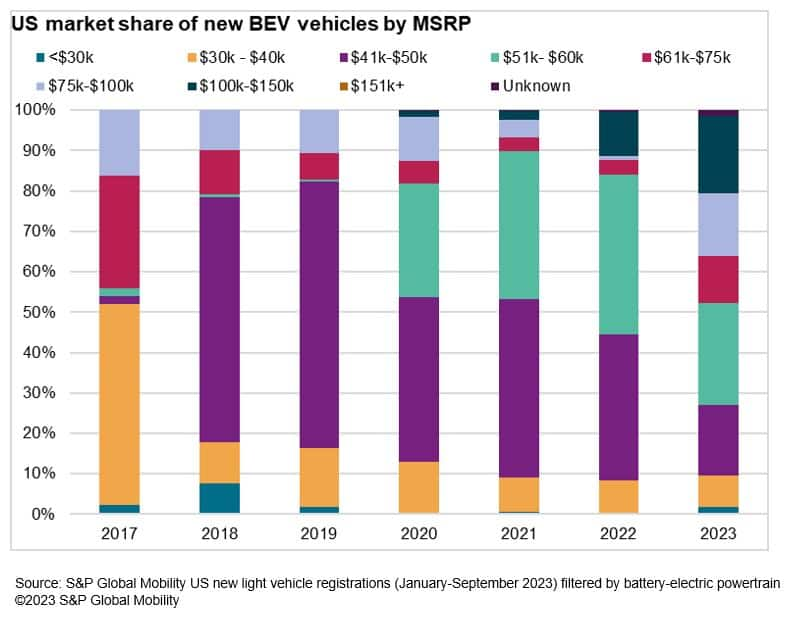

As the global market electrifies, finding

inexpensive EVs remains a challenge. Most OEMs are building

premium-priced EVs to better amortize costs before aiming for

economies of scale. Fully-electric offerings only have three

affordable options (under $30,000 before incentives) currently in

the US market – the Chevrolet Bolt EV and Bolt EUV, and Nissan Leaf

S. And while the BEV market still represents a small fraction of

overall registrations, the lion’s share of BEV registrations

resides in the $41,000-$60,000 MSRP range – with few registered

below $40,000.

Consumers are already pushing back on the

affordability of electric vehicles. A recent S&P Global

Mobility survey of 8,000 EV owners and intenders worldwide

showed “affordability” to be the No. 1 reason against purchasing an

EV – more so than concerns about range anxiety and the charging

network.

Opening the door to mainland Chinese

automakers

This exiting of the entry segment by legacy

OEMs could open the door for low-price models to enter the US and

European markets via non-traditional channels. In the US market,

those vehicles could be designed by mainland Chinese automakers,

but built in and imported from Mexico – thereby exempting them from

the 25% tariff levied on vehicles assembled in China.

The same applies to the market situation in

Europe – not only with affordable, internal-combustion vehicles,

but also in the nascent affordable electric vehicle niche. While

European automakers scramble to find profitable ways to build

affordable EVs, mainland Chinese OEMs have already started

penetrating the market.

So far, low-cost EV offerings are limited –

which could open the door in the EV space to brands such as NIO

(from mainland China), VinFast (from Vietnam), and others planning

on entering the US market. Some Chinese EV brands have already made

inroads in Europe – including the familiar MG brand that SAIC

acquired in 2007 and since leveraged.

That scenario may soon change, however, as

legacy automakers deliver entries such as the Kia EV3 and

reimagined BEV Renault Twingo – the latter coming in below

€20,000.

Despite the temptations of the US market,

mainland Chinese OEMs may prefer easier markets to penetrate with

affordable cars, said Caroline Hu,

consulting principal for the APAC region for S&P Global

Mobility.

“Political issues and IRA regulations are not

beneficial to foreign brands. Also, the hot overseas areas (for

mainland Chinese automakers) are the European, Southeast Asian, and

Mexican markets,” Hu said.

S&P Global Mobility research of the ASEAN

market currently shows same-model prices in Thailand and Indonesia

are 1.8 to 2.2 times that of the selling price in mainland China,

because it includes import taxes and logistics fees. The same

applies to the European market. But as mainland Chinese brands

start building factories in overseas markets, vehicle prices will

decrease accordingly.

“Chinese brands are trying to build a brand

image for intelligent, high-quality, high-performance vehicles –

not just cheaper,” Hu said.

A quick comeback?

Forecasts aside, the A- and B-segments in

Europe tend to be relatively cyclical, and there could be a slight

sales rebound for opportunistic players, said Calum MacRae,

director of research and analysis for S&P Global Mobility

Automotive Supply Chain and Technology.

For example, Renault had refreshed its Clio

supermini as a more-expensive, hybrid-only hatchback earlier this

year. But citing cost-of-living pressures of its demographic

target, in October Renault announced a gas-only version priced at

£17,795 in the UK, a £3,500 price cut from the hybrid model (prices

for the gas model vary on the Continent, from €21,950 in Germany to

€23,400 in France, but still represent a substantial price cut from

the hybrid).

“Renault won’t be alone in recognizing the

opportunity presented by the current dearth of affordable small

cars in the market,” MacRae said. “Others may follow, not just

because of a market share opportunity, but it also fits the

narrative of helping entry buyers in a cost-of-living crisis.

However, in a segment where margins are consistently razor thin,

the opportunity to do this profitably may quickly pass if others

jump in.”

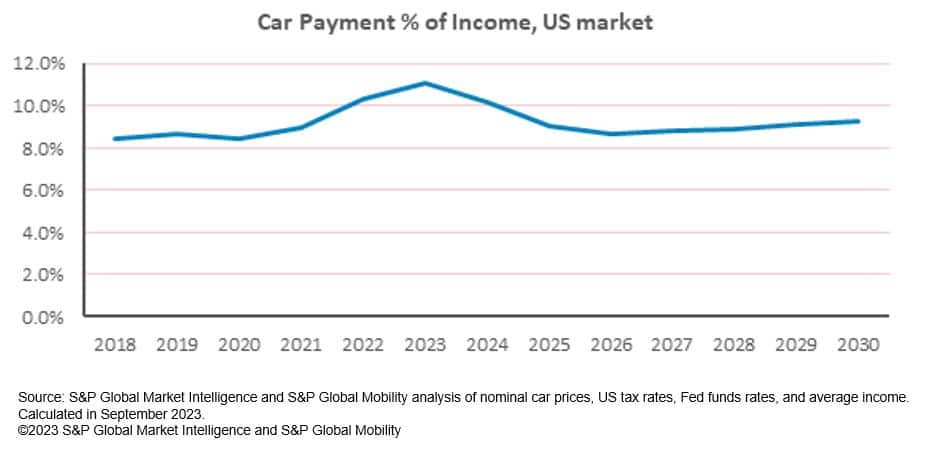

Affordability is more than

price

Of course, the vehicle transaction price is

only one part of affordability, as consumers also need to consider

incentives, trade-in value, taxes, fuel economy, and loan rates.

But at its core, average annual car payments as a percent of income

began to rise in 2021 and have continued to climb through 2023.

Multiple factors contributed to the increase, including:

-

Slower income growth rates beginning in

2022; -

Steady growth in vehicle prices;

-

Significantly lower purchase incentives;

-

Elevated vehicle loan rates prompted by Fed

funds rate hikes.

Looking ahead, US income growth and incentives

are expected to marginally increase. Average vehicle pricing will

remain a factor of body style and powertrain system mix. One silver

lining: As OEMs begin attaining economies of scale in electric

vehicle production, the consumer should benefit from lower vehicle

prices.

Then there is leasing, often seen as the

entryway for those households with Maserati tastes but Mazda

budgets. But leasing of vehicles sits at less than 19% of total

transactions year-to-date in 2023, compared to 30% in 2019. Leasing

has been less attractive for these affordable models – especially

considering incentives have instead prioritized the leasing of

electric vehicles as inventories and model choice improve.

“EV leasing has jumped since April, as a

potential relief valve on some of these constraints once production

levels improve,” said Peter Nagle,

associate director of research and analysis for S&P Global

Mobility. Also, BEV inventories are rising, prompting the

possibility of aggressive incentives from legacy OEMs to match

several rounds of price cuts by Tesla. There also will be the

benefit of cash incentives (rather than tax breaks) directly from

the US government starting in 2024, Nagle added.

“Incentives have been moving higher, and

inventory levels are returning to traditional levels,” Nagle said.

“Some very attractive financing terms are returning for outgoing

models that have elevated inventories.”

That said, affordability concerns are expected

to linger as interest rates and prices remain elevated.

————————————————————–

Dive deeper into these mobility insights:

CONNECT WITH OUR MARKET STRATEGY

TEAM

AUTOMOTIVE PLANNING AND

FORECASTING

WEBINAR: EV OUTLOOK AND PRICING

(EUROPE)

SIGN UP FOR OUR TOP 10 TRENDS

MONTHLY NEWSLETTER

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.

[ad_2]