56% of adults feel ‘behind’ on retirement savings, survey finds. Here’s how to tell if you are

[ad_1]

Peter Cade | Stone | Getty Images

Plenty of people feel like they are behind on their retirement savings. But what exactly does “behind” mean?

More than half, 56%, of American adults in the workforce say they are behind where they should be when it comes to saving for their retirement, including 37% who reported feeling “significantly behind,” according to a new Bankrate survey. Nearly a third say they would need $1 million or more to retire comfortably.

Here’s how experts say you can figure out if you’re actually behind — and what you can do to catch up.

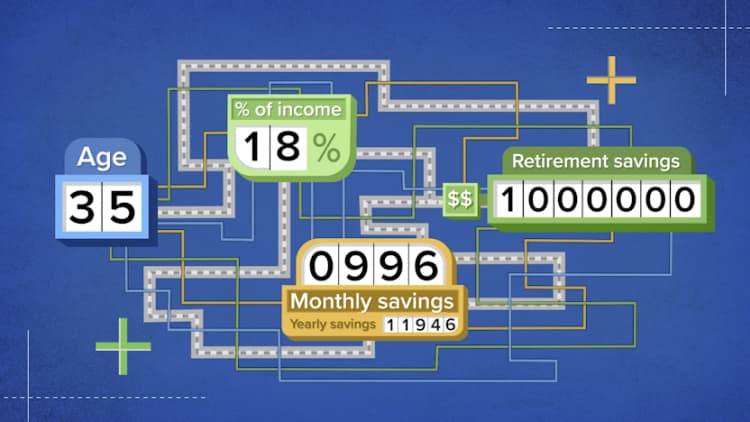

Online tools can provide points of comparison

Adults may feel behind because they haven’t reached “these goals in their minds as either rules of thumbs or points of comparison” that they’ve set for themselves based on what they read online, said certified financial planner Lazetta Rainey Braxton, co-founder and co-CEO of virtual advisory firm 2050 Wealth Partners.

Braxton, a member of the CNBC Financial Advisor Council, pointed to the “numerous calculators” available online to help investors gauge how much they might need, factoring in both ongoing lifestyle expenses and those that may increase in retirement, such as medical costs. The latter can be significant: According to Fidelity, the average retired couple age 65 this year may need around $315,000 saved to cover health-care expenses in retirement.

Brokerage firms such as Fidelity and T. Rowe provide benchmarks to help clarify the path to retirement. The benchmarks provide different age milestones and a target for how much to save.

For example, according to Fidelity’s guide, you should aim to have twice your starting salary saved by the age of 35, and 10 times your starting salary by the age of 67. According to T. Rowe, you should have 1 to 1.5 times your current annual salary saved by age 35, and anywhere from 7 to 13.5 times your salary by age 65.

‘Specific information is better than no information’

Based on such measures, it’s no wonder people feel behind. People between 25 and 34 years old have an average 401(k) balance of $30,017, or a median $11,357, according to Vanguard’s How America Saves Report 2023. Even in the 55- to 64-year-old age group, the average and median balances are $207,874 and $71,168, respectively.

Comparing yourself against benchmarks might make adults near or in retirement stressed if they are told that they need an additional six-figure sum to retire, Christine Benz, director of personal finance and retirement planning at Morningstar, told CNBC.

“But I do think specific information is better than no information,” Benz said, of benchmarks.

Generation Xers and baby boomers reported feeling more behind on their retirement than anyone else in the Bankrate survey, with 51% of Gen Xers and 40% of boomers thinking they are “significantly behind.”

Bankrate senior industry analyst Ted Rossman said older adults feel more behind because if they have not yet retired, it is getting closer, and these workers are realizing “that they don’t have as much saved as they would like.”

People are also living longer on average, which means many workers are now needing to finance what could be a 30-year retirement. In that case, Rossman said a 4% withdrawal rate was a “safe bet.” If people believe they need between $1 million and $2 million to retire — as 13% said in the Bankrate survey — then a 4% withdrawal rate would equate to approximately $40,000 per year, he said.

“It doesn’t start to sound like quite as much and then it’s like, ‘Oh, wow, I might need more than $40,000 a year to live on,'” Rossman said. “So now that’s why you’re feeling behind.”

How to catch up on retirement savings

Oftentimes, looking at so many different places for savings guidance may only cause more anxiety, said CFP Marguerita Cheng, CEO of Blue Ocean Global Wealth in Gaithersburg, Maryland.

Cheng — who is also a member of CNBC’s Financial Advisor Council — said that if your employer retirement plan sponsor’s website and multiple other tools indicate you are behind, the next best thing to do is to look at your contribution rates.

When people say they are maxing out on their retirement plan, they often mean they are maxing out in terms of their employer’s match, which usually hovers between 5% and 6%, Cheng noted.

However, you may be able to contribute more to your 401(k) to meet the annual maximum, she said. Workers can contribute up to $22,500 this year under the IRS’ 2023 limit. Those age 50 and older — who reported the most stress about their retirement — are eligible to contribute an additional $7,500.

While Bankrate found that this age group is also the least likely to know how much they need to retire, Rossman said people who don’t have quite as much time left should not be discouraged from getting started on or adding to their retirement savings.

For younger workers, early moves to start investing and boost contributions can help them stay on track. Gen Zers and millennials reported feeling the most ahead on their retirement savings, Bankrate found.

Rossman stressed that “every dollar” you save in your 20s or 30s counts since “time is on your side.” If young people start early and see gains compound by around 10% per year, their money could “double five times over 35 years,” he said.

“That’s a big difference.”

[ad_2]